MAX Policy is a collection of provocative ideas and policy solutions generated by the minds at the Max Bell School of Public Policy.

Could a carbon tax make CanadaÔÇÖs tax system more efficient?

I am asking and answering this question as a conservative. I prefer taxing consumption over taxing income. I prefer lower taxes over higher taxes. I prefer flatter taxes over steeply progressive taxes. And I prefer smaller government over bigger government.

Canadian conservatives (and their political counterparts) have almost made a sport of fighting carbon taxes. Entire political have been waged against . They have done this primarily by opposing tax increases as a way to fight climate change. But what if a shift to carbon taxes could meet conservative goals of taxing consumption, flattening taxes and slowing the growth of government?

This paper asks whether carbon taxes can make the tax system more efficient while ignoring whether or not carbon taxes are the right tool for addressing climate change. This is not an ideological argument ÔÇô a more efficient tax system will be better for the economy and raise revenues for the government in ways that minimize distortions in the economy.

I make three stand-alone arguments for a carbon tax. First, that a carbon tax is one way to reduce taxes on savings and investment. Second, that a carbon tax can eliminate the economic distortions of a progressive income tax on employment decisions. And third, that a carbon tax is an opportunity to tax something that is shrinking rather than, as we do now, tax things that are growing.

Climate change doesnÔÇÖt even enter into my argument. I make an argument for carbon taxes without even mentioning climate change (for the record, I believe carbon taxes are a superior way to address climate change).

The first step in making this case is to examine the mix of taxes Canada currently uses to raise revenues.

CanadaÔÇÖs current tax mix

What is CanadaÔÇÖs current tax mix?

The question is complicated by the fact that Canada has a large federal government and also large provincial governments, so the tax mix is different across the country. Alberta has no sales tax while some provinces collect up to a third of their own-source revenues from sales taxes.

I therefore look at the overall Canadian tax mix ÔÇô ignoring those provincial differences. This has the added advantage of washing out CanadaÔÇÖs significant inter-governmental transfer system. rolls up those differences and compares CanadaÔÇÖs tax mix to that of other G7 countries and the OECD average. On this table, Carbon taxes fall into the ÔÇťOther ConsumptionÔÇŁ category.

|

: Tax Revenues as a Percent of Total Revenues |

|||||||||

|

╠ř |

Canada |

US |

Germany |

UK |

France |

Japan |

Italy |

G7 |

OECD |

|

PIT |

36.3 |

40.3 |

26.6 |

27.4 |

18.8 |

18.6 |

25.8 |

27.7 |

23.8 |

|

CIT |

10.5 |

7.6 |

5.2 |

8.3 |

4.5 |

12.0 |

5.0 |

7.6 |

9.0 |

|

Payroll |

14.9 |

24.0 |

37.6 |

18.9 |

36.8 |

40.4 |

30.1 |

29.0 |

26.2 |

|

Property |

12.0 |

11.1 |

2.8 |

12.6 |

9.4 |

8.3 |

6.6 |

9.0 |

5.7 |

|

Value Added Tax |

13.5 |

0.0 |

18.5 |

20.8 |

15.2 |

13.3 |

14.4 |

13.7 |

20.2 |

|

Other Consumption |

9.7 |

16.9 |

8.6 |

11.5 |

9.2 |

7.1 |

13.8 |

11.0 |

12.5 |

|

Other |

3.2 |

0.0 |

0.6 |

0.5 |

6.2 |

0.3 |

4.4 |

2.2 |

2.6 |

A few observations: First, Canada, like the United States, relies relatively heavily on personal income taxes and relatively lightly on payroll taxes compared to other G7 countries and especially the OECD average. Second, Canada, again like the United States, relies less on value added taxes and consumption taxes than Europe and the broader basket of OECD countries. Third, Canada relies more heavily on corporate income taxes than its G7 counterparts and OECD nations.

If Canada were to rely more heavily on carbon taxes and less heavily on income taxes, it would shift CanadaÔÇÖs tax mix towards the average of other developed countries. It would make Canada less unique, from a tax mix perspective.

And that is precisely the question we will ask: Should Canada consider a revenue neutral shift toward more carbon taxes? As Ken McKenzie from the University of Calgary , ÔÇťthere is no compelling reason why the size of the government sector should expand in conjunction with the introduction of a carbon tax.ÔÇŁ

We restrict our answer here to efficiency, while ignoring important questions about equity or fairness. Which isnÔÇÖt to say such questions are not important: they are. But our focus will be on the economic efficiency of the tax system.

The efficiency of a tax system is tied to the economic distortions caused by that system. An efficient tax system will raise a given amount of revenue with the least economic distortions. Economic decisions made in the presence of a more efficient tax system will be closer to economic decisions made in the absence of any taxes at all.

Shift taxes from income to consumption

The first way a carbon tax can make our tax system more efficient is to tax consumption instead of income. Jack Mintz, also from the University of Calgary, ÔÇťn│▄│ż▒░¨┤ă│▄▓§ showÔÇŽ higher growth rates have been associated with less reliance on corporate and personal income taxes compared to consumption taxes.ÔÇŁ

Why are consumption taxes more efficient and more growth-friendly than income taxes? Consumption taxes tax only what is consumed, not what is invested or saved. Taxing savings or investments reduces their rate of return. This biases decisions in favour of spending today rather than saving or investing and thereby spending tomorrow. And less investment today means lower growth in the future.

Think of it this way: when you tax savings or investment, the interest rate at which these decisions should, from an efficiency perspective, be made . To the extent that corporate income taxes reduce the funds available to the firm to invest, it has the same effect ÔÇô decisions are biased in favour of spending today rather than investing for the future.

This is less of a problem for the Canadian personal income tax, which CanadianÔÇÖs largest sources of personal savings: Registered Retirement Savings Plans and principal residences. And our personal income tax system also provides tax breaks for education savings (Registered Education Savings Plans), disability savings (Registered Disability Savings Plan) and just plain old savings (Tax-Free Savings Accounts). All of these plans allow after-tax savings to grow tax free, reducing economic distortions to savings decisions.

CanadaÔÇÖs personal income tax system therefore mimics a consumption tax for the vast majority of Canadians. Only those who save beyond the alphabet soup of tax deferral plans (RRSPs, RESPs, RDSPs and TFSAs) and/or their principal residence see their savings taxed ÔÇô that is, only the wealthiest and/or the most parsimonious. And this is on top of very generous treatment of small business income that many wealthy Canadians use to shelter their savings.

So, if we want our tax system to shift further towards consumption and away from taxing savings and investment, we should focus on reducing the corporate income tax. This is all the more urgent as CanadaÔÇÖs corporate income tax appears to be compared to its key competitors ÔÇô not surprising as we tend to rely on it to a greater extent than other countries (Table 1).

A further shift toward more consumption taxation would make our tax system more efficient. But is a carbon tax a consumption tax? Some economists get quite at the very suggestion. Yet, if a consumption tax is a tax that avoids taxing savings or investment, a carbon tax is clearly a consumption tax. A carbon tax is levied on things that are consumed, not saved. So a shift from taxation on savings or investment to a carbon tax will reduce the distortion associated with taxing savings or investment.

Some may object that a broad-based consumption tax--a value-added tax like the GST/HST for example--is more efficient than a carbon tax. But our conclusion remains true even if we could get a greater efficiency gain from relying less on corporate income taxes and more on a broader-based consumption tax. The question we are asking here isnÔÇÖt how we can design the most efficient tax system, the question is how we can design a more efficient tax system. And shifting tax from corporate income to carbon could make our tax system more efficient.

Flatten the tax system

A second argument for carbon taxes is that they are an opportunity to remove some of the distortions our personal income tax system has on the decision to work. High tax rates are a key source of economic distortion in individualsÔÇÖ decision to work.

These distortions operate in two offsetting ways. As tax rates rise, it makes taxed activity, like work, relatively less valuable than non-taxed activity, like leisure and family time. So as tax rates rise people will do less of one type of activity (work) than the other (leisure or family time) than they would if tax rates were lower. This distortion is called the substitution effect.

On the flip side, a rise in tax rates makes leisure and family time more costly because it means you need to work more to maintain your income. So as tax rates rise, people will work more to sustain their standard of living than they would if tax rates were lower. This distortion is called the income effect.

These two effects sometimes cancel each other out. Indeed, most ÔÇô though by no means all ÔÇô studies suggest that men shift their labour supply very little in response to changes in tax rates. On balance, show that when men face higher taxes the relatively higher value of leisure is cancelled out by their need to keep their income stable.

This typical finding for men as a whole, however, masks important differences between men. As menÔÇÖs , they become increasingly receptive to the substitution effect and reduce their labour-force participation. And under a progressive tax system rates rise as income rises and magnifies those distortions. To put the point starkly, if the sole goal of the tax system was to minimize these kinds of economic distortions (it isnÔÇÖt, of course) then tax rates should fall as income rises, not the other way around.

These effects are larger for women. In particular, rising tax rates reinforce patriarchal pressure by pushing to reduce their labour-force participation in favour of (most often) family time. These effects are larger for married women and even higher for married women with kids. And these effects grow as incomes and tax rates rise.

The deleterious effects of higher tax rates are reinforced when comparing to lower tax countries, with the former showing less work and employment and economic growth than the latter.

To sum up, a more steeply progressive income tax is, on balance, more economically distorting than a less progressive tax. This statement remains true even if you believe that a more progressive tax is fairer ÔÇô which it certainly is. All we are saying here is that there is a cost to that fairness and that a flatter tax is less economically distorting than a progressive tax.

Carbon taxes are flat taxes. The rate you pay is entirely independent of your income level. It therefore follows that if we were to replace some of our progressive income taxes with carbon taxes, the result would be a less progressive tax system overall, and thereby a less economically distorting tax system overall.

Which is not to say that carbon taxes arenÔÇÖt distorting in different ways. A carbon tax is economically distorting in how it taxes consumption ÔÇô it taxes some consumption at higher effective rates than other consumption. from the University of Ottawa has evaluated the impact of a $30 (per tonne) carbon tax on the price of various goods. He estimates that a carbon tax will increase the cost of services by about one percent while raising the cost of electricity by eight percent and natural gas by eighteen percent. (This is also true of a sales tax which, like the GST/HST, exempts certain items from tax. Food and childrenÔÇÖs clothing, for example, are taxed at zero while everything else faces the tax.)

These distortions between different types of consumption are different in nature than income or substitution effects. Higher-income individuals pay the same carbon or sales tax as lower-income individuals for the same goods or services. It may distort their choices between which things to purchase (groceries which are exempt versus restaurant food which is not, or higher-carbon goods versus lower-carbon goods), but not how much or whether to work.

And so we circle back to our previous point that shifting away from a progressive income tax and toward a carbon tax will reduce the economic distortions on employment for, especially, higher income men, and women who are married or have kids.

Slow the growth of taxes

The third way a carbon tax can improve the efficiency of the tax system is that it can slow the growth of government. Or to frame it in the form of a question: Should a tax system automatically collect greater amounts of revenue, either per person or as a share of the economy?

There are at least four reasons to think it should not. First, to continue the point in the last section, higher taxes are more distorting than lower taxes, so we should avoid taxes that automatically rise. Second, rising taxes mean a larger government and, without getting into the debate over the , at the limit we cannot allow our government to grow indefinitely. Third, there is an argument for diminishing returns to government spending versus private sector spending. And fourth, automatic tax increases imply a democratic deficit ÔÇô it gives politicians a larger and larger pot of money without giving voters a say on whether those politicians should have a larger pot of money.

The Canadian tax system, if left entirely alone over time, will collect more per person and gobble up a larger share of our economy. And that is true even if you adjust for inflation.

Note that I am not making an argument about the . No matter what starting point you pick for the size of the Canadian government, the current tax mix means our tax system will automatically increase governmentÔÇÖs size. We are talking here about growth in taxes not the current level of taxes.

The tax system collects inexorably more for two reasons. First, our primary tax bases are growing faster than our population and our economy. This is accelerated, in the second place, because of the effect of a progressive income tax in a world where higher incomes are growing faster than lower incomes.

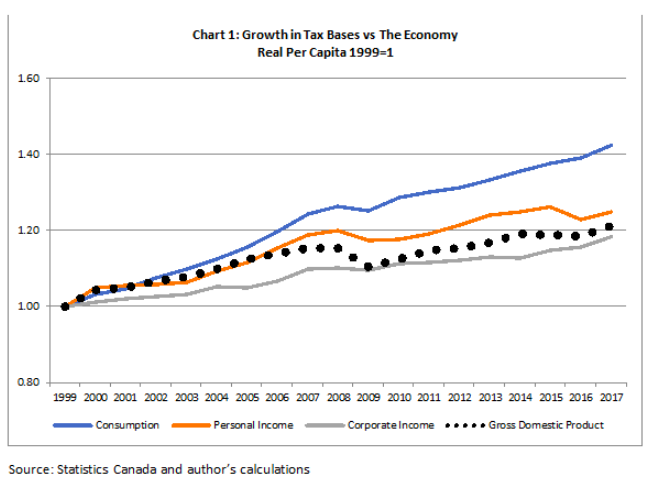

Chart 1 plots the path of consumption, personal income and corporate income in Canada for the past twenty years. It plots the size of the tax bases ÔÇô not the revenues themselves ÔÇô used for each of CanadaÔÇÖs major sources of revenue.

In real per capita terms consumption has grown by 42 percent, personal income by 25 percent, and corporate income by 18 percent over the past 20 years. This means that government revenues from a pure flat tax on consumption would have grown in real per capita terms by 42 percent since 1999. A pure flat tax on personal income would raise 25 percent more per capita today than twenty years ago.

╠ř

╠ř

There is not, of course, a pure flat tax on all income ÔÇô which would mean the same percent tax on the first dollar as the last dollar you make, no matter how much you make. Canada has a progressive income-tax system, where tax rates rise as income rises.

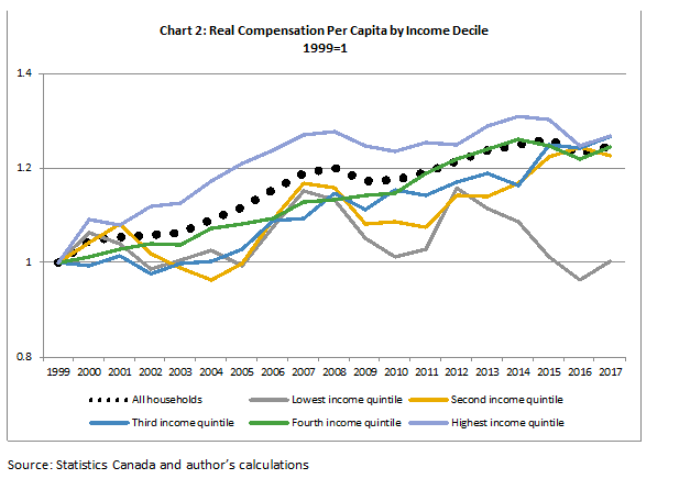

Since 1999, income for poorer Canadians has remained constant in real per person terms while income for richer Canadians has risen (See Chart 2). A progressive income-tax system will therefore mean revenues growing faster than 25 percent in real per capita terms ÔÇô as a progressive income tax means we collect proportionally than the poor. We are collecting more revenues from those whose incomes are growing faster and less revenues from those whose incomes are growing slower.

╠ř

╠ř

Perhaps holding tax revenues constant in real per capita terms is unrealistic ÔÇô wages and incomes also grow in per capita terms and governments spend a lot of money paying wages and sustaining incomes. So perhaps revenues (and thus the size of government) should grow in real per capita terms.

But should government revenues grow faster than the overall economy? At the limit, the answer is obviously no ÔÇô we cannot turn the entire productive resources of our economy over to the government.

Chart 1 also includes real per capita GDP. The Canadian economy has grown 21 percent in real per capita terms since 1999. This means that a flat tax on consumption or a flat tax on income would result in government revenues growing faster than the economy since 1999 while a flat tax on corporate income would have grown less than the economy over this time.

Almost three quarters (from Table 1) of Canadian government revenues come from taxing personal income (PIT and payroll) or consumption. In short, the very design of the Canadian tax system means that, if tax rates were held static, revenues would automatically grow faster than the Canadian economy.

Carbon taxes, on the other hand, should shrink over time, both in per capita terms and in relation to the size of the Canadian economy. In fact, as they say, that is a feature of carbon taxes, not a bug. A $30 (per tonne) carbon price would by between 10 and 20 percent over the next decade, with carbon revenues coming down accordingly.

And this holds even if we plan to continually raise carbon taxes over time, so long as each increase in carbon taxes is entirely offset by a reduction in one of these other faster-growing tax bases. So long as the tax base on which we are shifting towards (carbon) grows slower than the tax base we are shifting away from (income or total consumption), the result will be lower overall taxes (and smaller overall government) under carbon taxes than under income or consumption taxes.

Increasing government reliance on carbon taxes while at the same time reducing government reliance on personal income, payroll or broad consumption taxes would therefore reduce the automatic long-term increase in government revenues that is a reality of the current Canadian tax system.

Concluding thoughts

A carbon tax would make the Canadian tax system more economically efficient for three reasons. First, if we taxed carbon more and corporate income less, our tax system would tax consumption more and savings and investment less. Second, if we taxed carbon more and personal income tax less we would flatten the tax system and reduce the labour-force distortions caused by personal income taxes. Finally, if we taxed carbon more and broad consumption or personal income less, our tax system would consume less per capita and less of the overall economy. Taxing carbon offers a way to slow an inexorable growth of taxesÔÇŽ and government.

As a conservative, I welcome the opportunity a carbon tax provides to tax consumption more, to flatten taxes overall, and to slow the growth of government.

We have thus far ignored entirely the question of fairness. And while it is beyond the scope of this paper, I will conclude by pointing out that there are two ways to address the fairness of any tax system. We can change how we raise taxes, such as by making income taxes progressive or exempting food from the GST/HST. Or we can change how we spend the money raised by taxes, such as by providing income transfers or tax credits to individuals or families.

Or to put it a different way, just because a change to the tax system in the name of greater efficiency makes it less fair (or less progressive) doesnÔÇÖt mean that change should be abandoned. It might mean, instead, that we use some of the revenues from that now more efficient tax system to address those fairness challenges.

Which is precisely what every Canadian jurisdiction with a carbon tax has done. And any future introduction of a carbon tax should also be fair ÔÇô indeed, it wonÔÇÖt succeed politically if it isnÔÇÖt.

And so I will conclude with this. Even if carbon taxes did nothing for climate change, we should still raise carbon taxes while lowering other taxes. Why? Because it will improve the efficiency of our tax system and slow the automatic growth in taxesÔÇŽ and government.

About the Author

Ken Boessenkool is the J.W. McConnell Professor of Practice at the Max Bell School of Public Policy at ¤ŃŻÂ╩ËĂÁ.

He is also a Research Fellow at the CD Howe Institute, contributor to The Line and President and founder of Sidicus Consulting Ltd.

Until recently, Ken was a founding partner of Kool Topp & Guy Public Affairs with Don Guy and Brian Topp. In the course of his career, he has served as Senior Counsel at GCI Canada, was Senior Vice President and National Practice Director for Public Affairs at Hill & Knowlton Canada, where he was also General Manager for Alberta and Manager of Business Development. Ken was a senior regulatory economist with two electricity firms. He once worked at a bank.

Ken has played senior strategic and policy roles in four national election campaigns for the Conservative Party of Canada under the leadership of Prime Minister Stephen Harper. He has been Chief of Staff to former Premier of British Columbia Christy Clark, a senior policy advisor to three national Conservative leaders, two Alberta Finance Ministers, and an Ontario Progressive Conservative Leader. He has played senior policy or campaign manager roles in three national leadership campaigns and three provincial leadership campaigns.

Ken is the Board Chair of Sonshine Community Foundation ÔÇô a Calgary based women and childrenÔÇÖs shelter. He has served on the following boards: The Canada-Israel Committee; The Cantos Music Foundation (now the National Music Centre); The Canadian Friends of Hebrew University, Civitas and the Forum of Federations.

Ken has published numerous policy and academic papers on a range of key national issues and is a frequent contributor to numerous online and print publications.